While conventional wisdom holds that B2B startups are the safer choice, is this really the case? Let’s delve into why a consumer-focused GenAI startup might actually be your golden ticket.

In 2023, the startup landscape of GenAI applications experienced a remarkable surge, propelled by the advent of ChatGPT and foundational models such as GPT-4 and Anthropic. Over the past year, venture capital has invested at least $21 billion into GenAI, and most GenAI applications have primarily targeted on B2B, particularly productivity improvement. In the latest Y Combinator batch, 65% of the startups fall within the B2B SaaS and enterprise sectors, whereas only 11% are focused on consumer-oriented verticals. The most popular product form is AI assistant.

Current Challenges in B2B GenAI

However, as we transition into 2024, it has become evident that a lot of startups in the domain are facing significant challenges. A majority of these B2B GenAI companies are grappling with financial losses and are frequently pivoting in an attempt to find product market fit.

Many startup founders struggle to convert Proof-of-Concept contracts into full annual agreements, often facing significant limitations in their bargaining power over pricing. Despite the $21 billion VC investment, GenAI startup only generated around $1 billion in revenue.

Heavy competition is one of the main challenges for startups in converting Proof-of-Concept contracts. But why is there such a strong focus on productivity improvement applications? The reasons are multifaceted and stem from various technology and market dynamics:

First, it is related to the nature of the current foundational models. Foundation models such as GPT-4 are the result of significant research breakthroughs and depend extensively on benchmarks that have been established within the academic community. Historically, these benchmarks have predominantly focused on knowledge-based tasks. For example, the benchmarks used in the GPT-4 technical report primarily consist of academic tests. Essentially, what we are creating with these models are entities akin to exceptionally skilled students or professors. This orientation naturally steers generative AI applications toward productivity enhancements. Consequently, it’s not surprising that students are the primary users of many AI-assisted products like copilots.

Second, there is a B2B-first culture in the American startup ecosystem. The American startup ecosystem has predominantly favored B2B ventures, with the consumer sector receiving significantly less investment over the past decade. Startup founders in US are afraid to build consumer startups. Although other countries such as China do not exhibit this fixed mindset, the U.S. has been a global leader in generative AI research and substantially influencing trends worldwide.

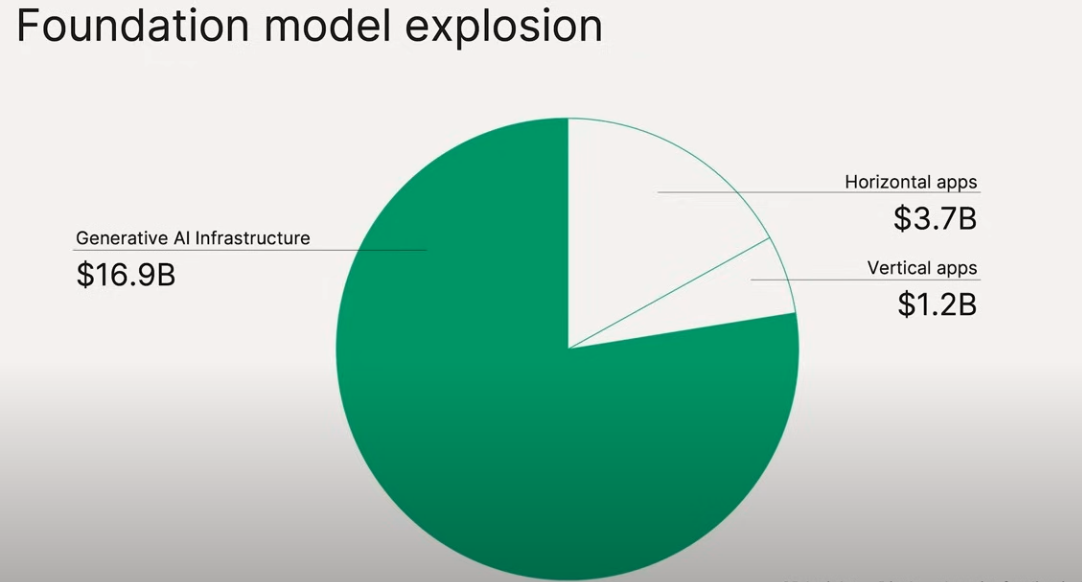

Third, the GenAI infrastructure boom levels the playing field for everyone. In 2023, the majority of investments were directed towards GenAI infrastructure, with many investment firms likening it to a “gold rush.” There’s a prevailing belief that, much like the merchants who sold supplies during a gold rush, those who provide the essential tools and services will profit first. The following figure shows that $16.9B out of the $21B billion VC money was spent on GenAI infrastructure. Newer players can always leverage better infrastructure.

Source: Sequoia Capital’s AI Ascent 2024 opening remarks

Due to the factors mentioned above, competition among productivity-focused GenAI applications is intense, undermining the ability of startups in this space to extract value from customers. As a result, the entire ecosystem remains predominantly financed by venture capital.

The Untapped Potential of Consumer GenAI

History often repeats itself. During the Internet boom of the 1990s, emphasis was initially placed on B2B applications. However, it turned out that the integration of the Internet into business contexts would take longer than anticipated. Salesforce pioneered the SaaS model, but it took nearly a decade to reach the $1 billion revenue milestone. In contrast, consumer applications have proven to be a quicker avenue for both creating and capturing value.

Google, Facebook, and Amazon have each developed consumer products that serve billions of people, discovering unique methods to monetize the internet by reaching vast audiences cost-effectively. Additionally, this approach has proven to be an effective strategy for building strong competitive advantages, or moats.

Strategies for Success

The 7-power framework is a crucial tool for analyzing business opportunities, identifying seven key levers: Scale Economies, Network Economies, Counter-Positioning, Switching Costs, Branding, Cornered Resource, and Process Power. For B2B GenAI startups,

Counter-Positioning and Process Power are typically the only levers B2B GenAI startups can pull due to incumbents holding advantages in the other areas. In contrast, Consumer GenAI startups have the potential to develop competitive moats across almost all these powers, providing numerous strategic advantages — especially if your founding team has strong technical capability in AI models and infrastructure.

It’s crucial for Consumer GenAI companies to own their AI models and infrastructure. This ownership not only fosters the development of Scale and Network Economies but also secures Cornered Resources, enhancing competitive advantage and market positioning.

On the one hand, to create a successful consumer app, controlling costs is crucial. Historical trends in developing larger and more powerful models have made them unsuitable for consumer applications due to high costs as the lifetime value (LTV) of consumer use-cases is typically much lower. For example, the LTV of a user is often just $20-30 but might ask hundreds of questions. However, utilizing all the tokens in GPT-4 can cost approximately $1.28 for a single call. Developing in-house expertise to create models that are both powerful and cost-effective is crucial to bridge the gap.

The good thing is that consumer applications are usually much more tolerant to hallucination, and might not need the most powerful model. In addition, the evolution of open-source models has enabled startups to develop their own models cost-effectively. With the recent launch of LLaMa 3, its 8B small model has outperformed the largest model from LLaMa 2. Additionally, there is anticipation that the 400B model, currently in training, will match the performance of GPT-4. These advancements make it feasible for startups to create high-performing models at a fraction of the cost associated with proprietary models. While significant investment is still necessary to reduce costs sufficiently to support large-scale consumer applications.

On the other hand, current foundational models are not ideally suited for creating robust consumer applications, as most large language models lack personalization and long-term memory capabilities. Developing new foundational models or adapting existing ones to better suit consumer needs is a critical challenge that Consumer GenAI startups must address.

Despite these challenges, startups that successfully tackle these issues can secure a significant competitive edge and establish long-lasting market dominance.

Thanks for reading this article and hope the article is useful for you. If you have any questions or thoughts, please don’t hesitate to comment or message me at jing@jingconan.com 🤗